Mining and Metallurgy

Africa has abundant natural resources which include Critical Raw Materials (CRM) which are fundamental to the modern economies of other countries. Further, among the CRM are the critical earth minerals which are critical to high tech industry and are geostrategic in the highly industrialized countries because of the major role these elements play in defense, aerospace, security and the lack of domestic supplies in most industrialized countries. The critical minerals include the platinum-group metals (PGM), indium, cobalt, manganese, tungsten, germanium, niobium, tantalum, gallium, antimony and the rare-earth elements (REE) or rare earth metal (REM). The REE are one of a set of seventeen chemical elements in the periodic table and include cerium (Ce), dysprosium (Dy), erbium (Er), europium (Eu), gadolinium (Gd), holmium (Ho), lanthanum (La), lutetium (Lu), neodymium (Nd), praseodymium (Pr), promethium (Pm), samarium (Sm), scandium (Sc), terbium (Tb), thulium (Tm), ytterbium (Yb), and yttrium (Y).

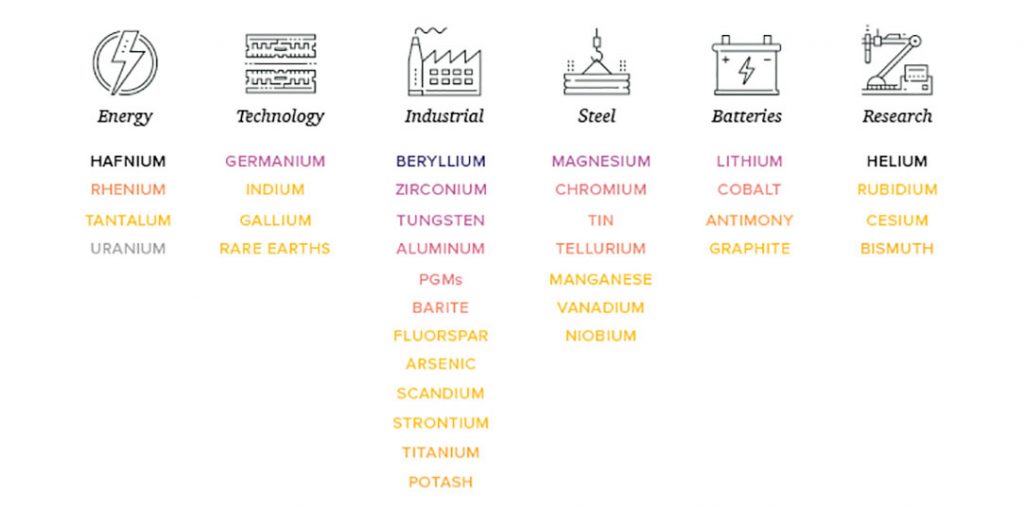

Uses of Critical Minerals and Rare Earth Elements

The critical and rare earth minerals are used for so many commercial applications and are are considered essential to a country’s national security and economic well-being. They are especially critical for the economies of the US, Japan, Europe and other industrialized countries. They are especially geostrategic as they are critically essential in high tech applications in defence, aerospace and security industries. For example Yttrium and praseodymium are what make smartphones so small, powerful and bright. In the defence industry, rare earths are vital in laser, radar, sonar, night-vision systems, missile guidance, smart bombs, jet engines, and even the alloys on armoured vehicles. Because rare earths are used for so many commercial applications, the US, Japan, Europe and other countries could be vulnerable to supply disruptions. Rare earths are considered essential to a country’s national security and economic well-being.

Some key uses of Critical Minerals and Rare Earth Elements

Africa’s significance and potential in World mineral trade

The mineral industry of Africa is the largest mineral industry in the world. Africa is the second largest continent, with 30 million km² of land, which implies large quantities of resources. For many African countries, mineral exploration and production constitute significant parts of their economies and remain keys to economic growth. Africa is richly endowed with mineral reserves and ranks first or second in quantity of world reserves of bauxite, cobalt, industrial diamond, phosphate rock, platinum-group metals (PGM), vermiculite, and zirconium.[1] Gold mining is Africa’s main mining resource. It is also a major source of, manganese, tantalium, and tungsten. Most of the worlds Tantalium comes from the Great Lakes Region, Mozambique and Ethiopia, and most of the world’s manganese comes from South Africa, Gabon and China. Africa offers the greatest potential for rare earth production, especially in South Africa, Tanzania, Malawi and Mozambique. Kenya, Burundi, Zambia and Namibia are also mentioned. Six of the world’s top 10 cobalt mines are in the DRC.

Further, Africa offers great potential for rare earth production, especially in South Africa, Tanzania, Malawi and Mozambique. Kenya, Burundi, Zambia and Namibia are also mentioned. Significant quantities of neodymium, praseodymium and dysprosium have been found in South Africa. The Steenkampskraal mine in the Western Cape province of South Africa has the highest grades of these REE in the world and with this South Africa hopes to become a significant supplier of rare earths in world markets.

So how does Africa benefit, leverage or derive advantage from its mineral endowment? It can not without advancing and supporting science, engineering and technology at all levels and involving all segments of society. Africa can get more from its minerals by building industries to service mines and generating a scientific knowledge base. Some economic and industrialization perspectives are advanced by Vuyo Mjimba in his article published in The Conversation – October 16, 2018.

Africa can get more from its minerals by building industries to service mines

Vuyo Mjimba – Chief Research Specialist, Human Sciences Research Council

Multinational firms from Europe, North America and more recently China still dominate the extraction and refining of most of minerals mined in Africa with minimal roles for African firms. From these minerals, foreign manufacturing firms produce consumer and industrial goods for sale in global markets at much higher prices than what’s paid for the raw materials. This is a source of lots of angst among policymakers and economists who are calling for increased local participation in the mining industry.

African governments are routinely advised to add value to their own natural resources to drive economic development. This is presented as a way of getting a slice of the huge returns enjoyed by others at the expense of countries in which the minerals are mined. This seemingly obvious reasoning is the basis of a growing policy focus on mineral beneficiation which involves improving the economic value of a mineral by turning it into a final or intermediate product.

The argument sounds logical. But accessing the rewards of this approach isn’t that simple. Those in favour of beneficiation tend to ignore the complexity of industry and markets of beneficiated products and the rules and regulations of supply chains. Most products, components and operations of the beneficiation industry and markets are currently alien to many African economies.

This means that, for the moment, beneficiation remains out of reach.

Take the case of steel. To use steel to manufacture washing machines for global markets, a country would need to either establish its own brands and outcompete established ones, such as Samsung, Defy and Hisense, or, alternatively, supply these popular producers with components. In Africa, this is unlikely to happen immediately because of small markets and brand loyalty among other challenges.

This is not to say that adding value to mineral resources shouldn’t be part of the agenda for African countries. But the focus should be elsewhere – the production of input goods like machinery, spares and services that support processes that precede beneficiation – exploration, mine construction and extraction itself. These are known as backward linkage industries and are ready for picking. This approach served countries such as the US and Norway where they gave rise to globally competitive manufacturing and services industries serving the mining and oil industries.

What’s missing in Africa

A critical hurdle to Africa developing a strong industrial base – a prerequisite for any beneficiation – is the dominance of China and other Asian countries in the labour intensive manufacturing sector.

So why can’t African countries simply emulate China?

A number of factors aided China in its industrialisation drive. Firstly, China is one country with a huge unified market that can produce and consume its own manufacturing output in addition to exporting the same goods.

Africa, for its part, is a continent made up of many countries. This market is fragmented which limits inter and intra country production.

Secondly, China has invested heavily in human capital and well as hard infrastructure such as bridges and roads. All these factors are critical for any major industrialisation drive – and beneficiation – but are lacking in the majority of African countries.

Refocusing

A greater focus on the production of input goods could yield better results. This is because it offers an easier development path that’s within technical grasp of many African countries.

The scale of Africa’s mining industry means that it has a ready made market for input goods and services. This includes the supply of heavy mining spares and consumables, contract mining as well as security and catering services.

It makes business sense to have the input goods and services of these activities close to where they are needed. Close proximity gives African companies an advantage over multinational mining firms. Even more critical, proximity reduces the need for the mining industry to hold huge inventories of imported spares and consumables – a nightmare for cash flow.

Industries developed to support mines isn’t alien to the continent. For example the supply of ball-mills that crush the ore-bearing rock in the ore processing plants is established in some Africa countries i.e. South Africa, Zambia and Zimbabwe. This small start could be expanded, in both scope and magnitude relatively easily.

Recommending that African countries focus on the processes that precede mineral beneficiation isn’t hypothetical. The historical experiences of the US and Norway, for example, confirm the positive stimulus that these processes had for the overall industrialisation journeys of these countries. The two countries transformed within 30 years to be leading suppliers of mining inputs that include mine dump trucks and drill rigs.

African states can follow the same strategy, with the necessary adjustments, and harvest the low hanging fruits of resource endowment, leap-frogging to achieve the same over a shorter period.